The Case for Mr. DIY

Plus! A side story to give a little context for this analysis

In this study:

Mr. Do it Yourself

History and business model

Profitability

Valuation

Why Invest?

Conclusion

Mr. Do it Yourself!

Mr. D.I.Y., a home improvement & hardware retail company, was first publicly traded on 26 October 2020 in Bursa Malaysia, and it was one of the hotly anticipated stock for investors as the IPO funding at RM 1.5 billion was the largest in three years with the only listing to surpass a billion ringgit in 2020. The attraction for the stocks primarily comes from its competitive standing (High operating margin) and the exponential growth in physical store presence across Malaysia.

In this blog post, I will lay out structurally about the company as a whole and will provide valuation based on four metrics to see whether the stock is overvalued or undervalued. Cases for positive or negative stories on the company’s future prospect are equally strong, but the tailwind coming from inside shareholders (Brokers and traders) are tilting towards higher stock price in the near term. Hence, even if my conclusion is to sell, it will be hard to see the stock price fall below the current share price because there is not enough momentum to depress the share price.

History and business model.

At that time, it was around 5 p.m. when I was just studying for my university exam. My laptop charger cord and the socket were all placed on the left side of where I sit, so if I stand up and walk left, my toe can easily touch and drag the cord together with the computer. Stupidly, I had my cup filled with water that was placed on the left-hand side of my computer. It was at that moment where I stand up, walk left, toe hits the cord and drag the computer together with the cup, water started flooding my laptop’s keyboard.

Clearly, I know the laptop was not going to function anymore (Power button not responding), but at least I would try to find out what was happening inside the computer. To do that, I needed some tools (screwdrivers etc.) to open the hardware, and that is where I find it most frustrating. Around my area (within 1km radius and I stayed in an area that are quite populous), there was NO shops that sell hardware products and the closest store that do sell was quite far away. That is when I remembered how convenient it was back in Malaysia where people would know that one retail shop that would sell hardware tools, whether in a shopping mall or stand-alone retail that are close to them, which is Mr. D.I.Y.

The company was founded by Tan Yu Yeh and the first store opened in 2005. Though I could not find any stories behind what drives him to start opening a hardware store, the company has then expanded its retail shop in shopping malls like Tesco and Aeon. Furthermore, it has expanded its store presence into local communities where the company has become a one-stop centre for home improvement and hardware products in the local area. This strategy was laid out by Andy Chin, who is now a marketing VP at Mr. D.I.Y. He told people that Mr. D.I.Y. was actually “filling a gap in their businesses”1, which I completely agree with given the absence of hardware stores around my area at that time when my laptop broke down (I interpreted the VP statement as filling a gap in local areas that have little to no hardware stores to serve the local communities).

Its business model is no different to other retailers, but it is done with scale and scope. It derived its revenues primarily from two sources:

Brick-and-mortar sales: 99% of its sales are generated through selling home improvement and hardware products to customers in its physical stores across Malaysia

E-commerce: Currently it only accounts for 1% of its total sales, but the company is investing heavily in this segment (because of movement restrictions from Covid-19) which will take on more weights in the future

In addition to selling home improvement and hardware products, the company has been rolling out subsidiaries with different store concept like Mr. Toys and Mr. Dollar stores in 2020. Mr. Toys will be selling toys for children and Mr. Dollar will be selling consumable goods (F&B). Both stores only account for 2% and 5% respectively out of the 734 stores Mr. D.I.Y. operates in 2020 and it plans to open an additional 175 stores that includes Mr. D.I.Y. and the two subsidiaries.

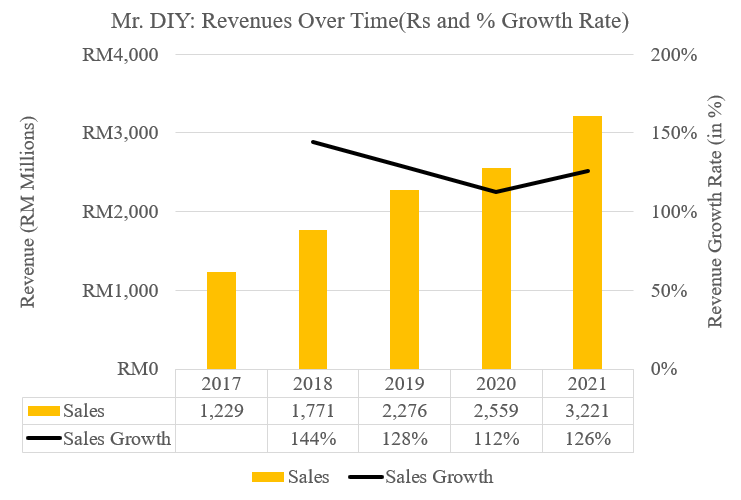

With such a strong market presence in Malaysia, Mr. D.I.Y. was able to maintain high level of revenue growth in 2020-21. Out of the 734 stores operated by the company, only 4 stores are stationed in Brunei, which means that it faces very little to no international operation risk as 99% of its stores is placed across Malaysia.

Even with the second competing retailer – One Stop Superstore – does not come close to Mr. D.I.Y. in terms of physical store presence in the country. Hence, it can generate strong revenue growth as the retailer has truly become the one-stop shop for home improvement and hardware products.

Profitability

Despite its fast store expansion coupled with rising COGS, Mr. D.I.Y. was able to maintain its operating margin above its peers across ASEAN. Notably, the company has seen its margin to fall in 2020 due to movement restrictions that causes its COGS expenses to increase (Wage and supply expenses) higher relative to its revenue growth.

Moving forward into the next decade, I don’t believe the company can maintain its high operating margin because of 3 reasons:

Rising competition on the e-commerce site for that sector will threaten Mr. D.I.Y. (due to lease obligation and staff remuneration) if the company still generate more than 90% of its revenue from brick-and-mortar stores

If the company continues with its expanding strategy over the next decade, inefficiencies will start to kick in in some stores where same sales store growth (SSSG) will decrease more relative to maintaining the store presence (2 Stores that are placed in proximity will compete for sales)

Sector revenue growth will wane as Covid driven demand will subside when economy recovers, and movement restrictions are lifted

Therefore, my projection for the company’s operating margin will fall from 23% in 2020 to 16% in 2030. This estimate is closely aligned to its ASEAN peers as Malaysia’s home improvement sector revenue growth will gradually decrease from the uptick demand during the Covid period, and the company starts to mature in generating consistent cash flow.

Valuation

I have adopted four key valuation metrics in this case analysis. Majority of the metrics suggest the current share price RM 3.90 as of 20th August is reaching its peak. However, analyst consensus believes the stock still have rooms to appreciate further, even though the stock price has gained more than 100% since its IPO inception in 2020.

Based on the DCF, the intrinsic value that I got is RM 2.51 which is -36% discount to the current share price at RM 3.90. My recommendation here is clearly to sell the stock based on the DCF, but we know the block traders (Brokers) have more influence in the stock price movement than my sell trade. Hence, if the brokers do not lower their target, I do not think the stock price will fall up to RM 2.51.

Below, you will see all the DCF estimation in the next decade up to the terminal years to show you my rationale on computing the assumptions and stories to come up with the FCFF2:

Why invest?

There are twofold as to why the stock is a good buy, even if its overvalued:

Its ROE at 17.9% in 2020 is much higher than its peers and my cost of equity, which suggest that Mr. D.I.Y. is generating significant value to shareholders as its reinvestment in expanding more physical stores is paying off

As of 2020, its profit margin stands at 14%. Assuming the company adhere to its dividend pay-out policy at 40%, and that the company can maintain that margin in the future and keep its cash flow consistent, it will be able to pay out 40% of its earnings to its shareholders.

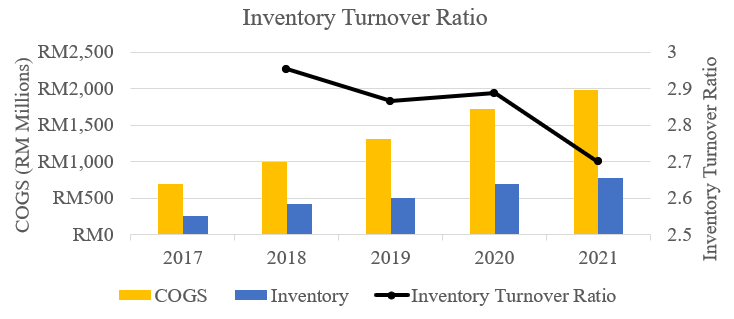

There will be a few firm-specific risks that you will carry if you choose to invest in Mr. D.I.Y. Specifically, the decreasing inventory turnover over the past year means that there are increasing inefficiencies in turning inventories into sales. Though the year 2020 was its lowest, analyst opines that the ratio will recover back to its pre-pandemic level in 2021.

On the minor front, majority ownership in Mr. D.I.Y. is held by Tan Yu Yeh and its family where the founder also sits in the board of director serving as Executive Vice Chairman. Holding more than 50% of the company’s equity, I worry that there will be increasing family-based decision making that will cause the company to make ventures that are non-core to the business operation. We have seen many times in Malaysian corporations that tries to make acquisitions or expanding new business ventures that are not related to the existing business operation (eg. Boustead Holding and Genting Group). Usually, these conglomerates use “diversification benefit” as the main driver to do value-destroying acquisitions, which is unnecessary because shareholders can do the diversification themselves.

Under the leadership of Chu Jin Ong - the CEO – I believe there will be no divergence in the company’s strategy to have the most physical store chain and largest market share in the home improvement sector in Malaysia. But if we were to start seeing the company getting into real estate investment or healthcare, it will be the starkest hint for shareholders to start trimming or selling the stock (It just does not make sense because they still have the e-commerce segment that have the most potential to grow their business, instead of delving into healthcare).

Conclusion

It might seem to you that my discussion and analysis lack conviction because my recommendation is to sell the stock, but I contradict my suggestion by placing more weights on the company’s potential growth and analyst consensus. Let me clarify myself here that I stand true to my suggestion where I will only go long when the stock price falls within RM 2.00 (± RM 5) to give me enough margin of safety at RM 2.51.

However, I (or we) must understand that the low interest rate environment and government stimulus have given brokers and traders excessive liquidity that chases too few stocks in the market. This is especially true to Mr. D.I.Y. when you consider the circumstances and its position at which it came into IPO, hence the stock price will stay persistently high because of the trade momentum that are driven by the brokers and retail traders.

Great growth story, decent management, but not a stock that is worth paying a premium for. Who knows when the stock price will fall to RM 2.51? Maybe it won’t at all in this short period of time when behavioural hubris is what we see from traders in this Mr. D.I.Y.’s skyrocketing stock price.

Video: YouTube Presentation

Dayangku, S. 2020, “In 15 Years, Mr DIY Grew From A Small KL Store To A Household Name Valued At RM10bil”, Vulcan Post, 23 October. Link: https://vulcanpost.com/719677/mr-diy-history-malaysia-home-improvement/

Excel file: https://docs.google.com/spreadsheets/d/16IT_NwkrEV65sBR_q0XiB2fW3DFiFEqX/edit?usp=sharing&ouid=111798043984751403895&rtpof=true&sd=true